We are dedicated to all aspects of taxation and related matters for our clients. With extensive experience in tax issues, we provide tailored solutions for both domestic and international transactions. Our services include strategic tax planning and litigation support, ensuring our clients receive informed guidance to optimise their tax positions and manage disputes effectively at all stages in the litigation process.

Navigating the complexities of tax assessments can be challenging. Our dedicated team is here to assist our clients through each stage of this process, ensuring they have the support they need to effectively manage disputes and optimise their tax position.

Typically, before issuing a Notice of Assessment, the MRA will issue a Contemplation letter to provide the taxpayer with an opportunity to submit explanations and documents.

At this stage, we offer full assistance to our clients by analysing the contemplation letter and by representing them in their negotiations with the MRA.

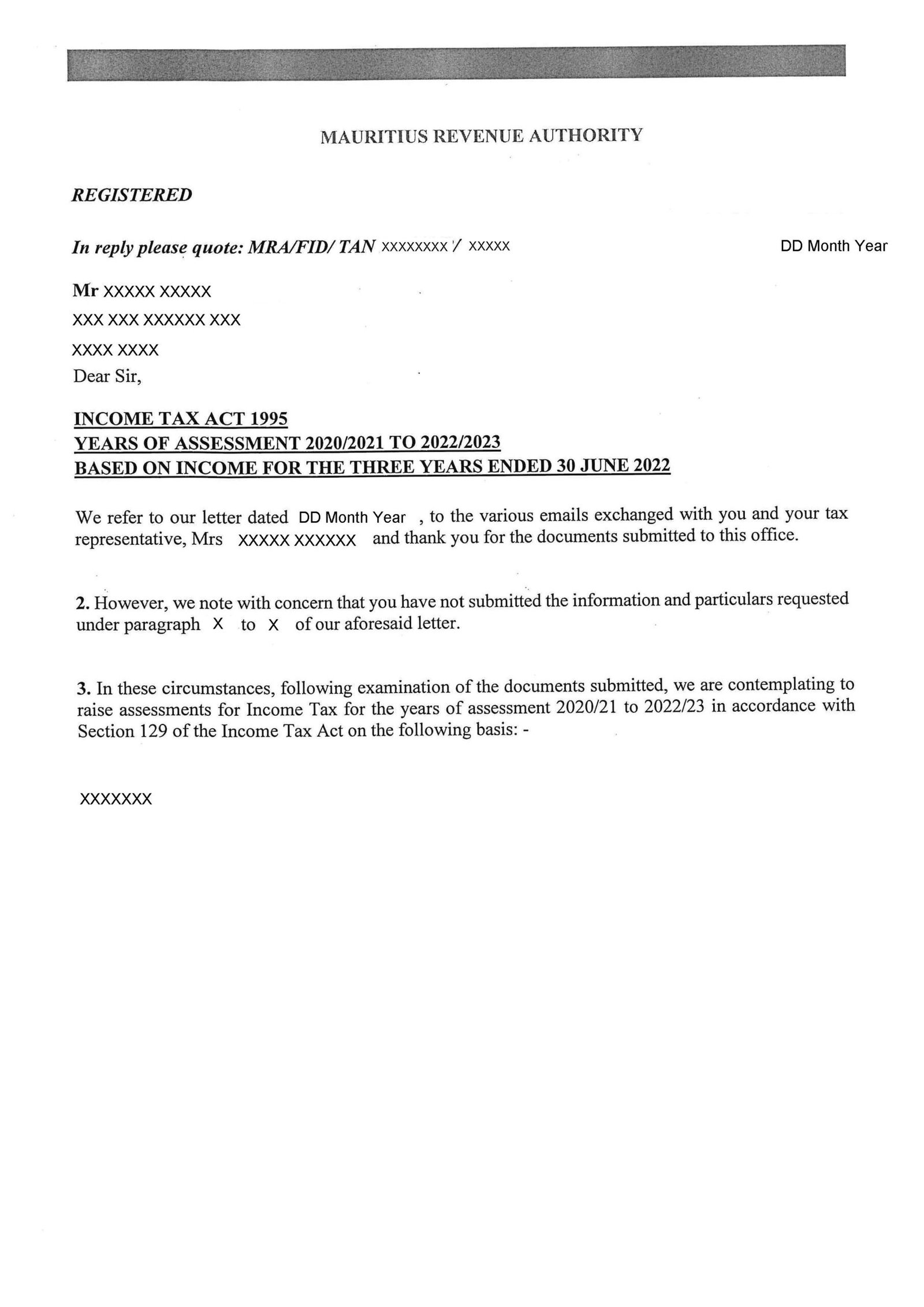

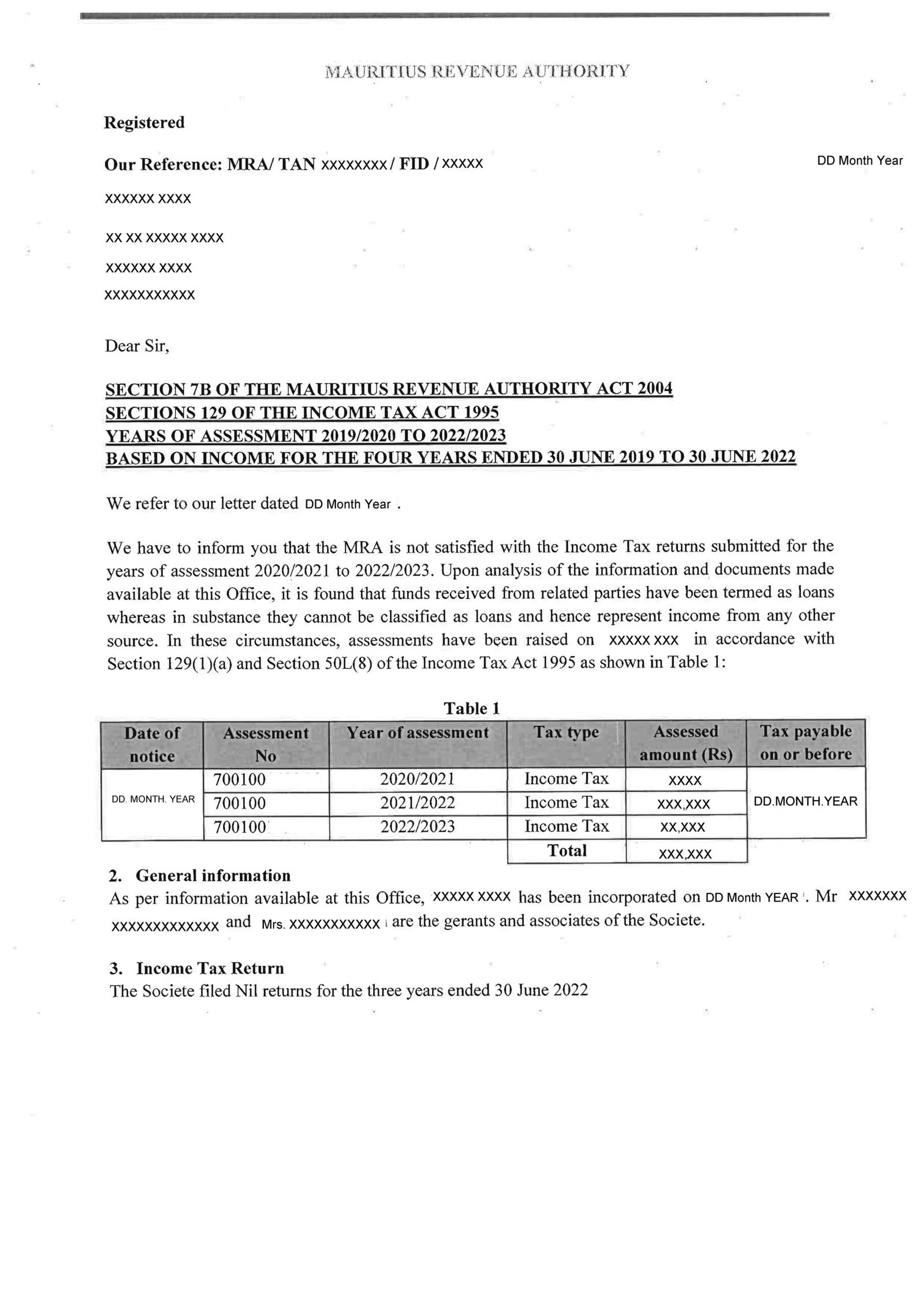

Typically, the revenue laws empower the Mauritius Revenue Authority (MRA) or the Registrar General to issue a Notice(s) of Assessment. The ‘Notice of Assessment’ essentially outlines the reasons and basis for the assessment and the outstanding tax payable.

At this stage, we assist our clients by analysing their Notice(s) of assessment and advising them on the way forward.

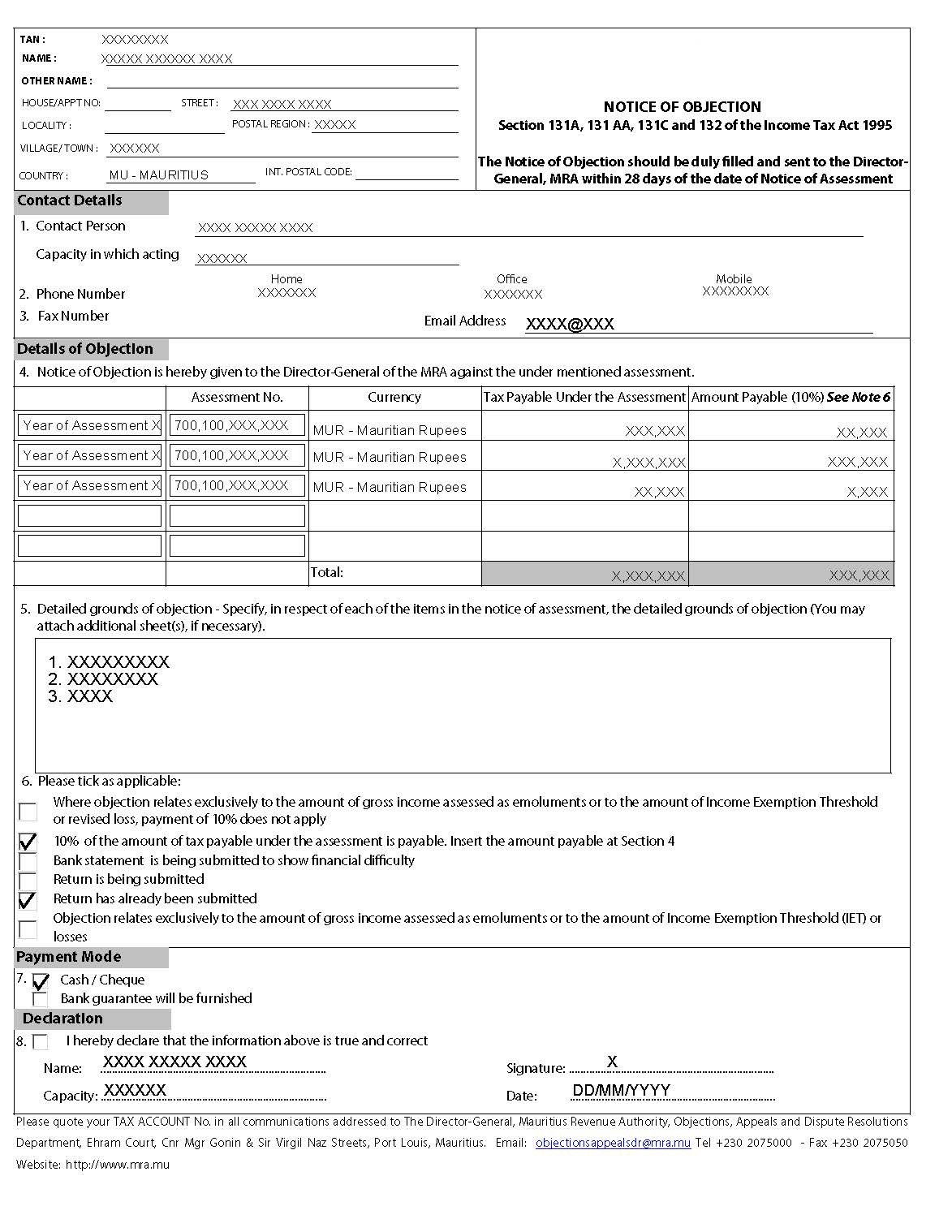

If you disagree with the assessment of the MRA or the Registrar General, you are required to file to the Director of the Objections, Appeals & Dispute Resolutions Department (OADRD) or the Registrar General as the case may be, a “Notice of Objection” form, stating clearly your reasons for disagreement to the assessment.

Of note here, you have only 28 days of the date of Notice of Assessment to lodge your objection to the assessment.

At this stage, we typically assist our clients throughout the objection procedure until a Notice of Determination is issued.

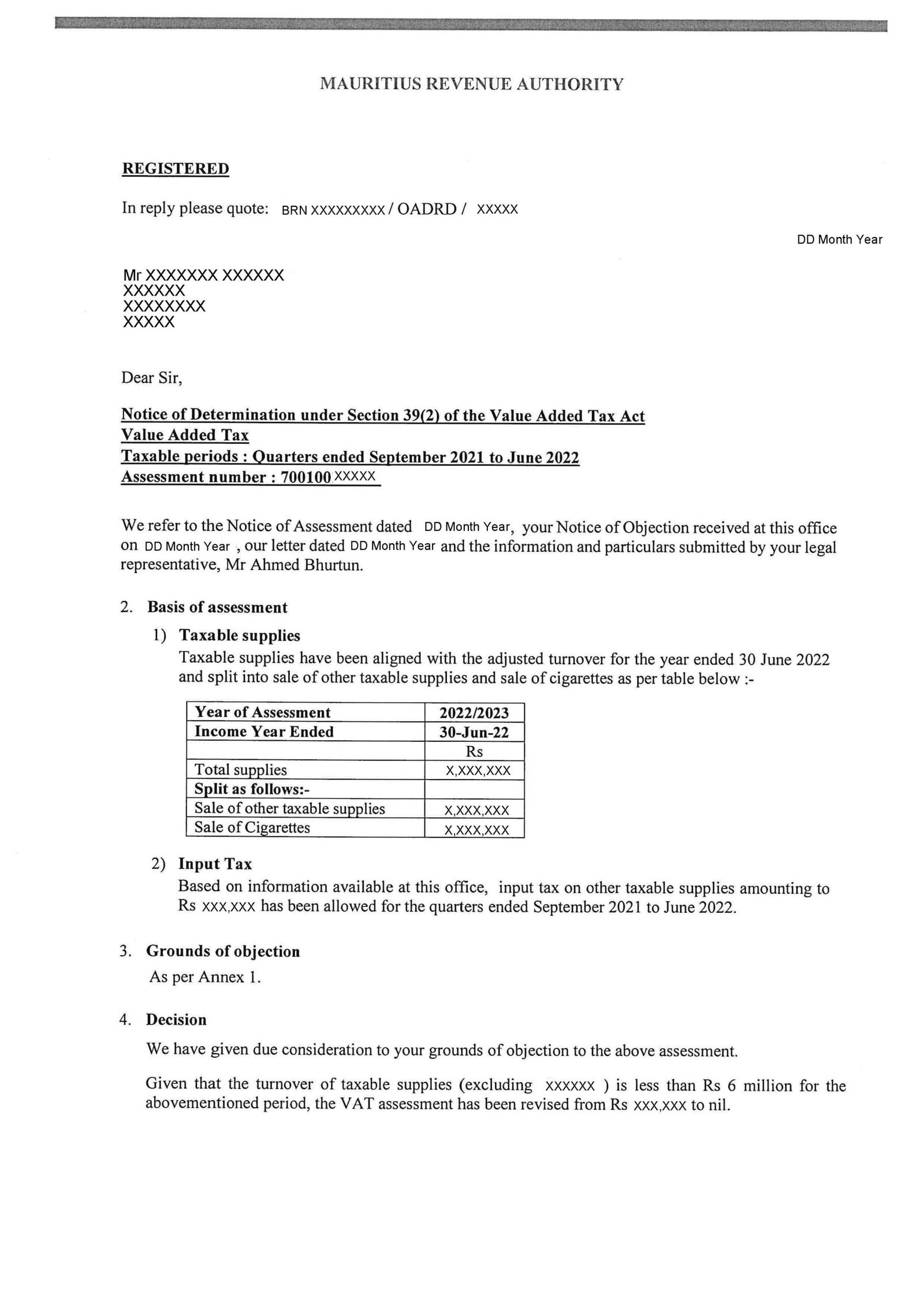

Once your objection is submitted, the OADRD or Registrar General will review it and issue a ‘Notice of Determination’. This document communicates their decision regarding the objection to the assessment.

At this stage, we analyse the Notice of Determination and advise our clients on the best way forward.

If you still feel aggrieved by the decision of the MRA or Registrar General in the Notice of Determination, you are required to make written representations to the Assessment Review Committee (ARC) within 28 days of receiving this notice. This is an opportunity to present your case for further consideration before a specialised committee.

At this stage, we assist our clients by drafting their written representations and lodging the same with the clerk of the ARC in a timely and professional manner.

Proceedings at the ARC take place before a panel consisting of the Chairperson or Vice-Chairperson and one or two expert members.

At this stage we assist our clients by meticulously preparing their case and providing them with expert representations before the ARC.

After hearing submissions from both sides and analysing any evidence on record, the ARC will deliver its decision.

If you feel aggrieved by the decision of the ARC, you have the right to appeal to the Supreme Court (SC) by way of case stated within 21 days of the date of the decision of the ARC.

At this stage, we assist our clients by working with an Attorney to lodge the appeal and providing them with robust representation before the Supreme Court.