Global Minimum Tax & the small island of Mauritius

Introduction

We are now in 2024 – the Year the Global Minimum Tax (GMT) is set to go live and dramatically transform the international tax landscape.

In view of contributing to the understanding of the GMT, we are pleased to share with you our short article which focuses on the history and the mechanics of the GMT, and its implications for Mauritius.

Historical development of the GMT

The concept of GMT is not a new one. In fact, it can be traced back to the early 1980s when countries began competing primarily on tax rates – the “Global race-to-the-bottom”. It then gradually gained widespread discussion and scrutiny as existing international tax structures, developed in the last century, began showing signs of weakness in the face of rising Globalisation and Digitalisation of the economy.

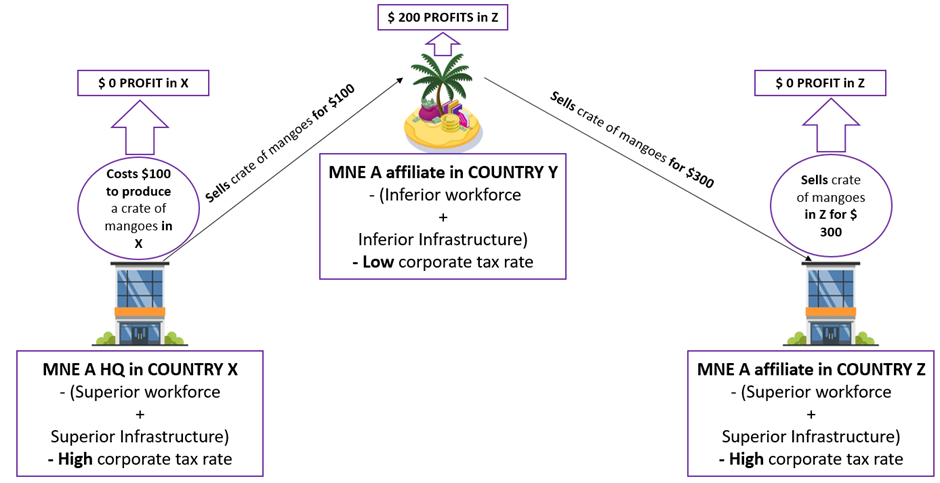

Indeed, with Globalisation, it became easier for multinational enterprises (MNEs) to minimise their tax obligations by operating in a particular Country or Countries (usually with superior infrastructures and workforce but high corporate tax rates) and then reporting their profits in another country (usually with inferior infrastructures and workforce but low corporate tax rates) using a technique called ‘Transfer pricing’. Consider the following example of a MNE A:

Fig. 1 – An example of profit-shifting by a MNE to its affiliate in a country with low corporate tax rate to minimise its tax obligations.

Digitalisation, for its part, made it possible for certain MNEs to offer their services (e.g. cloud storage, streaming services) to consumers around the world without the need for a physical presence in those countries. As existing international structures rely heavily on physical presence, it became difficult for governments to tax these types of MNEs.

These issues were brought into spotlight in the wake of COVID-19 pandemic when governments worldwide were struggling with revenue shortfalls and surges in public expenditure, forcing them to review the existing international tax structure in view of mobilising more resources.

It is in this spirit that in October 2021, over 135 countries (including Mauritius) agreed to a two-pillar solution to update the key elements of the international tax structure. While Pillar 1 is concerned with a better distribution of taxation of MNEs based on the country of operation, Pillar 2 aims to control tax competition on corporate profits by introducing a GMT of 15%. Of note, only Pillar 2 or the Global Anti-Base Erosion Model (GloBE) rules is of concern in this present article.

The mechanics of the GMT

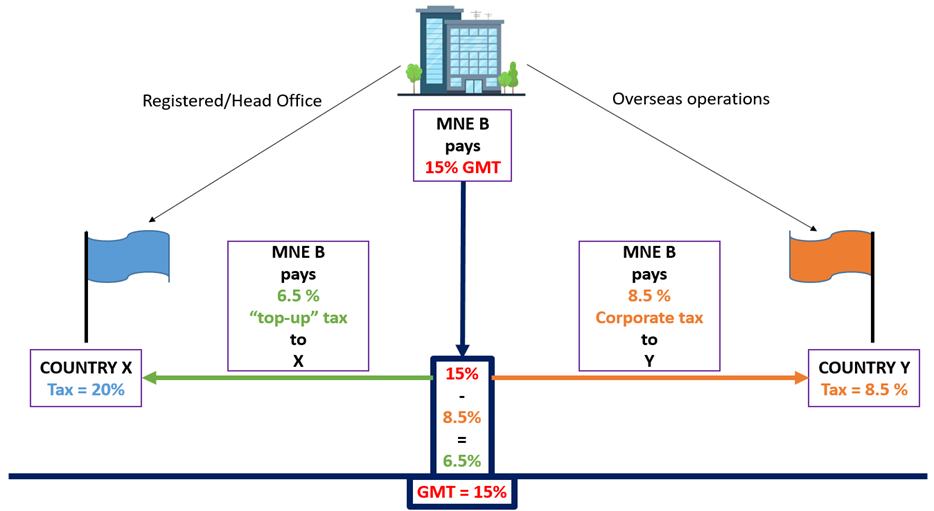

The Pillar 2/GloBE rules are designed to ensure that large MNEs with revenues exceeding €750M in at least two out of the last four years pay a base tax rate (GMT) of 15%, regardless of where they are operating from or declaring their profits in. It is aimed at preventing MNEs from engaging in profit-shifting (as in Fig. 1 above) or tax avoidance strategies. Consider the following example of a MNE B:

Fig. 2 – An example illustrating how the GMT works.

In the example above, notice how the “top-up” tax of 6.5% is paid to Country X, where the MNE is headquartered. However, this would be different if there was a Qualified Domestic Top-up tax (QDMTT) involved.

Article 10 of the GloBE rules provides for a QDMTT which jurisdictions are free to introduce or not. If implemented in a jurisdiction, QDMTT operates to ensure that any additional tax on economic activities in a jurisdiction that results from the GMT is to the benefit of the domestic jurisdiction.

What are the implications of a GMT for a small country like Mauritius?

Mauritius has already introduced the QDMTT under its domestic laws with the amendment of S.4 (Imposition of tax) of the Income Tax Act to add a new subsection 3 which reads:

“Notwithstanding the other provisions of this Act, a company forming part of an MNE group which is liable to a Top-up Tax in a year may be required by the Director-General to compute and pay a Qualified Domestic Minimum Top-up Tax in such form and manner as may be prescribed.”

As explained above, this will ensure that any top-up tax due from MNEs located in Mauritius will be paid in Mauritius itself, levelling the playing field with larger countries. Moreover, collecting tax through the Mauritian QDMTT will significantly reduce compliance burdens for MNEs by saving them from being subject to top-up taxes in other countries in respect of the operations in Mauritius. However, it is important to highlight that these will only be possible with the issue of prescribed Income Tax Regulations which will have to be based on the OECD Anti-Base Erosion Model Rules. Yet, this was not announced in last year’s budget speech and the Government has so far not provided a timeline for the implementation of the QDMTT.

Some have argued that the implementation of a GMT/QDMTT will seriously limit Mauritius’ capacity to use tax incentives as a tool to attract foreign investments and businesses. While this may be true, it remains that Mauritius can still compete on corporation tax rates for entities outside Pillar 2’s reach, that is, Mauritius’ 15% tax rate will still be attractive to businesses with annual revenues below €750M. Furthermore, despite being a small country, Mauritius possesses a strong legal framework, great infrastructures, a literate and dextrous labour market, an ideal geographical location, and sophisticated financial systems that it can still rely on to continue attracting foreign investments and businesses.

Conclusion

As the world is transforming its international tax landscape, the small island of Mauritius is faced with unique challenges but also presented with new opportunities. What awaits our small country is uncertain, but what is certain is that we are known to be resilient when faced with challenges and make the most out of opportunities presented to us.

Decisions Delivered by the Assessment Review Committee

- ESSAR COMMUNICATIONS LTD V/S DIRECTOR GENERAL-MRA ARC/IT/195-18

The Applicant in this case had made interest-free advances to one of its wholly owned subsidiaries (“the transaction”). The Respondent considered that the transaction had not been made at arm’s length and assessed the Applicant on deemed interest. The Applicant objected to this, but the assessment was maintained. Aggrieved, the Applicant made four grounds of representations before the ARC to the effect that:

- The Respondent was wrong to conclude that the Applicant should have applied a notional interest on the transaction.

- The Respondent failed to appreciate that the transaction did not have any characteristic of a loan.

- The Respondent was wrong to conclude that the provisions of S.75 of the Income Tax Act was applicable on the transaction.

- The Notional interest applied by the Respondent was grossly exaggerated.

The Committee began by considering ground 3 and noted that while both sides acknowledged that the issue has been decided in favour of the Respondent in Innodis Ltd v Director General, Mauritius Revenue Authority [2023 SCJ 73], the Applicant argued that the interpretation given to S.75 of the Income Tax Act in that case is wrong and must not be applied. The Committee, having regard to the decisions in Peerthy v Municipal Council of Vacoas-Phoenix & Anor [2022 SCJ 166] & Marie & Ors v Electoral Commissioner & Ors [2010 SCJ 138], considered that the decision of the Supreme Court in Innodis is binding, and it cannot depart from it. Accordingly, the Committee decided to set aside the ground 3.

The Committee then considered grounds 1 & 2 together which concerned the treatment of the amount advanced in the transaction. The Applicant argued that the amount advanced represented “Share application monies”, whilst the Respondent argued that it constituted a loan, which being interest-free, was not an arm length’s transaction. After a thorough analysis of the evidence submitted and the law, the committee concurred with the Respondent that it is important that the commercial and financial transactions between related parties are at arm’s length and that the Applicant should normally have applied a rate of interest on the amount advanced. The Committee accordingly decided to set aside grounds 1 & 2.

Finally, the committee took the view that ground 4 can hardly be taken to be a ground independent of grounds 1 to 3, and accordingly also set it aside.

With all grounds of representations set aside, the committee upheld the Respondent’s Notice of Determination.

- MR NASSER HANSYE V/S DIRECTOR GENERAL-MRA ARC/VAT/91-19

In this case, representations were made by the Applicant following a Notice of Assessment which gave a direction to the effect that according to section 15(1) of the VAT Act the Applicant ought to have been registered for VAT as its turnover of taxable supplies had exceeded the threshold amount.

The Applicant relied on S.19 of the MRA Act, S.39 and S.40 of the VAT Act – the latter of which provides for instances where the taxpayer can make representations to the Committee on VAT issues.

The Respondent contended that the representations were premature, and that the committee did not have jurisdiction to hear same.

Upon analysing S.40 of the VAT Act, the Committee found that there is an important issue which had to be dealt with and which does not fall within the two limbs of S.40 – whether the Applicant has designed any arrangement or transaction to directly avoid any VAT liability. Accordingly, the Committee concluded that this issue must be considered by the Objection Unit before it could give any further decision.

- MEDIC WORLD LTD V/S DIRECTOR-GENERAL-MRA ARC/IT/149-22

The Applicant in this case made representations to the ARC to the effect that Loan from third parties were classified as turnover by the Respondent instead of loan.

The Committee decided to set aside the ground of representations. In reaching this decision, the Committee took the view that it could not rely on mere letters from third parties whose evidence could not be put to test before the Committee as already established in earlier similar cases of Sundanum v Director-General, MRA (ARC/IT/110-10), Ganesh Rampat v Director-General, MRA (ARC/IT/114-08) and Greedharry v Director-General, MRA (ARC/IT/07-21).

- SACHIN BHIMJI PATEL & ORS V/S THE REGISTRAR-GENERAL ARC/RG/1373-18

The issue before the ARC here was whether a transfer of shares from the Applicant’s deceased grandfather to the Applicant attracted a Registration duty. The Applicant argued that the transfer was by an ascendant to a descendant and that therefore no registration duty was payable. The Respondent argued that the shares have been transferred by the succession of the deceased grandfather to the Applicant grandson and was accordingly not totally a transfer by an ascendant to a descendant.

The ARC agreed with the Respondent.

In reaching, their decision, the Committee first referred to Item 28 Part III to the first schedule of the Registration Duty Act which makes it clear that there are 3 instances that transfer of movable property (such as shares) will not attract Registration duty. (reproduced below):

- by an ascendant to a descendant or to the latter’s spouse or surviving spouse;

- between the heirs of a deceased person of movable property acquired by inheritance from that person; or

- between spouses.

The Committee then analysed the evidence on records and noted that there were 4 direct heirs (sons) of the deceased person. The Committee further noted that the Share Transfer Form bore the signatures of the 4 direct heirs (sons) of the deceased which made it clear that the deceased never transferred the shares to the grandson directly. The Committee also highlighted that, in any event, the deceased cannot effect any transfer. This led the Committee to conclude that the transfer of shares was actually between the 4 direct heirs (the succession) and the Applicant grandson in which case neither (a) nor even (b) in the above-reproduced law would be applicable.

The Committee went to highlight that since that in the absence of a Will, the shares were deemed to be divided equally among the 4 heirs.

Thus, the Committee concluded that the share of three of the 3 direct heirs (Applicant’s uncles) were deemed to be three quarter and only one quarter which is the share of the Applicant’s father transferred to him was exempted from Registration duty.

- LINDSAY TECK YONG V/S THE REGISTRAR-GENERAL ARC/RG/65-20

This was the first ARC decision for the year 2024 and concerned the non-payment of the statutory percentage of the claim before making an objection and before making representations to the ARC.

In this case, the Respondent addressed a letter to the Applicant asking for additional Land Transfer Tax in the sum of approximately Rs 90,000 in relation to a sale of property. The Applicant contended that the property in question was seized by the bank, and that therefore he was not the owner at the time of the sale, although it was made in his name as per an agreement between him and the bank. The Applicant subsequently filed his objections to the Respondent’s decision. However, as contended by the Respondent, he failed to pay the 10% of the claim for making an objection as prescribed under S.28(3)(a) of the Land (Duties and Taxes) Act. Interestingly, as also contended by the Respondent, the Applicant went on to make representations before the ARC, and this time failed to pay the 5% of the claim for making representations before the ARC as prescribed under S.28(4) of the Land (Duties and Taxes) Act.

After analysing the law in relation to objections and representations, the Committee concluded that the Applicant was under an obligation to pay the 10% first and it is only if the Registrar-General maintains the claim that he can make representations to the Committee. The Committee also highlighted it was not going to rule on the merit of the matter at this stage.

- FINE CRUSH LTD V/S DIRECTOR GENERAL-MRA ARC/EPF/01-18

This was a very interesting case concerning the Environment Protection Fee (EPF) under the Environment Protection Act (EPA).

The Applicant in this case was involved in stone crushing, manufacture and sales of premium quality construction materials, gravels, rocks and other aggregate-based materials or blocks. It also collected a fee which represented the transport cost of stone crushing product to clients who had ordered these materials.

The central issue before the ARC was whether the Applicant was liable to pay the EPF in relation to the transport fee, i.e. whether the turnover should include the transport cost. The Applicant argued that the purpose of the SS. 65 & 66 of the EPA was to impose an environmental tax on the basis of the activity which has an impact on the environment, and that any other activities undertaken by the entity in question which is not directly related to the environment protection need not be taken into consideration as far as the turnover of the entity is concerned, which in that case was the transport services.

The ARC took the view that the turnover should include the transport cost and accordingly set aside the representations. In reaching this decision, the ARC explained that the EPA speaks about designated enterprise instead of designated activity, and that the term enterprise stands for a business activity which comprises of different departments for its proper functioning. The ARC further explained that there was a clear link between the stone crushing activities and transport services in that the latter is an added service to sell the finish good to the ultimate buyer without the enterprise would not be able to function. The Committee also highlighted that the Applicant had even declared VAT on the amount that it had been charged for transport services offered to the buyer.

- IOX Cable Ltd V/S DIRECTOR GENERAL-MRA ARC/VAT/23-20

This was yet another case concerned with the non-payment of 10% and the subsequent lapsing of objection.

The contention of the Applicant was that it was unable to pay the 10% in relation to the objection filed with the Respondent because on insufficiency of funds.

The ARC was satisfied that the bank statements produced on behalf of the Applicant showed that there were indeed insufficient funds to satisfy the 10% requirement. The Committee further took note of the fact that the bank accounts were under attachment order and therefore the company was not able to pay the 10%. Accordingly, the Committee ordered the Respondent to look into the financial status of the Company and if funds were still not available to pay the initial amount, the Applicant to pay Rs 200,000 within one month to cover all the administrative expenses of the Respondent and to consider the objection. Otherwise, the full amount will have to be paid within one month, following which the Respondent would consider the Objection filed. [emphasis is ours]

The ARC highlighted that the approach adopted in this case was based on its specific circumstances and should not constitute a precedent.

Note: The Committee mentioned ‘within one month’ but did not specify as from which date. But it is likely that it meant ‘within one month as from the date of this decision’.

- ROGERS HOSPITALITY OPERATIONS LTD V/S THE REGISTRAR-GENERAL ARC/IT/003-22

This was a rather unique case in that the Representations to the ARC erroneously mentions the name of Rogers Hospitality Operations Ltd instead of Foresite Property Holding Ltd (the taxpayer in this case) which are two distinct entities forming part of the same group.

It was the Applicant’s case that it cannot be held responsible for the mistake in the representations filed in the name of Rogers as it had properly inserted the correct TAN and the BRN when it had filed its representations online with the ARC. On the other hand, the Respondent contended that the Applicant had wrongly filed the written representation which was filed online by the taxpayer although it had the correct TAN of Foresite.

After considering all the evidence on record, the Committee considered it wise to allow the Applicant 21 days as from the date of the ruling to file an amended representation.

Important Legislations and Legislative Amendments

- The Construction Industry Authority Act 2023

An Act to provide a consolidated legislation for the construction industry through the establishment of the Construction Industry Authority.

The Building Control Act and the Construction Industry Development Board Act are repealed.

The Construction Industry Authority would take over the functions and powers of the Building Control Advisory Council and the Construction Industry Development Board.

S.44 of the Act provides “Notwithstanding any other enactment, the Authority shall be exempt from the payment of any duty, charge and tax”.

The Act came into force on 11 December 2023.

- National Savings Fund (Collection of Contributions) (Amendment) Regulations 2023

In these regulations –”principal regulations” means the National Savings Fund (Collection of Contributions) Regulations 1997.

The First and Third Schedules to the principal regulations are revoked and replaced by the First and Third Schedules set out, respectively, in the First and Second Schedules to these regulations.

Regulations effective as from 1 July 2023.